Zimbabwean tax residents are subject to income tax on their earnings. The Income Tax Act (Chapter 23:06) provides the framework for determining taxable earnings and the rate of tax that is applicable to the earnings. It also provides details of income that is exempt from tax and deductions that are permitted in determining taxable earnings.

Employees are taxed on a monthly basis in terms of the pay-as-you-earn (PAYE) system. Tax is withheld at the source by an employer on taxable amounts paid to an employee. The tax tables operate on an escalating scale basis until a certain threshold is reached, after which a flat rate of tax applies. (The flat rate threshold is referred to as the Marginal Tax Rate (MTR).)

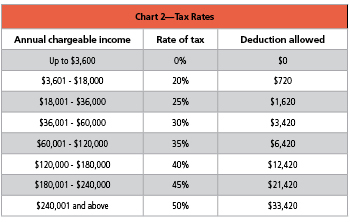

The annual rates of tax payable are listed in Chart 2.

As an example, if an employee receives annual taxable earnings of US$ 150,000, the PAYE to be withheld would be calculated as shown below:

US$ 150,000 x 40% - US$ 12,420 = US$ 47,580 (per annum)

The employer has a responsibility to withhold the correct PAYE and make payment to the Zimbabwe Revenue Authority (ZIMRA) by the 10th of the following month after the end of the month in which PAYE was deducted. The employer is also required to submit a return by the same date. The return can be submitted using the e-filing system (electronic submission for PAYE).

Employees are required to contribute toward a fund for AIDS. The AIDS Levy is calculated as a percentage of the individual’s taxable income. The current rate is 3%. Thus, an employee with a tax charge of US$ 5,074.15 would be charged US$ 152.22 for the AIDS Levy. The employer is tasked with the calculation and deduction of the AIDS Levy. The AIDS Levy is paid to ZIMRA along with the PAYE withheld.

National Social Security Authority Obligations and Filings

Employers are obliged to contribute on a monthly basis to the National Social Security Authority (NSSA, the National Pension Scheme) at a rate of 3.5% of an employee’s monthly earnings, with 3.5% being deducted from the employee’s earnings as his or her share of the contribution. There is an earnings ceiling limit in place that currently is set at US $700 per month (the limit is subject to change, and payroll professionals are encouraged to check amendments in legislation regularly to ensure that payroll calculations remain compliant). Contributions are made for all employees between the ages of 16 and 65.

Employers are required monthly to complete a Form P4A, which is a remittance form and ensures that contributions made for the period are correctly credited, and a Form P4, which provides a breakdown of employer and employee contributions.

When there is a new hire, employers will need to complete a Form P3 in the month in which the employee is paid their first earnings. For terminations of employment, a Form P4C is required to be completed. Contributions will be made in the normal manner up to the last day of employment.

Employers are required to ensure that records are maintained for each employee and are available on demand for inspection by an NSSA inspector. The information that needs to be provided during an inspection includes: the National Social Security number, the national identity number and full name of an employee, the employee’s date of birth, the date of commencement of employment, the date of termination of employment, the date and amount of total earnings (monthly/weekly/any other time period), the amount of the deduction from basic earnings in each contribution month, the employer’s contribution in respect of each month, and a summary record of the number of workers in employment per month with the associated total wage bill.

Accident Prevention and Workers Compensation (APWC)

Businesses in Zimbabwe are classified according to the industry in which they operate and each is allocated an industry code (IC). (The Sixth Schedule to Statutory Instrument 68 of 1990 contains the code listings.) Each industry is allocated an insurance premium rate that is determined as a result of annual risk analysis reviews. The rates are gazetted into law each year. Payroll professionals should review the NSSA website or Government printers’ websites to ensure that the correct rates are being used.

Employers are required to complete an annual wage declaration form (WC 50), which is used to assess the employer’s risk and will determine the rate the employer will pay the following year. The form is prepared by NSSA, and the employer is required to insert missing data.